Foreign currency risks are often undesirable, but unavoidable side effects of an internationally diversified portfolio. In this INSIGHT we give you an overview of how currency risks can be managed through currency overlay strategies. The low interest rate environment in Europe, which has now lasted for years, represents a major challenge for many European institutional investors to achieve their target return. In July 2012, the ECB deposit rate was at 0.00% for the first time; it has been negative since June 2014. (Source: European Central Bank 30.04.2019) In search of returns, many investors have diversified their portfolios internationally. This is due to higher return levels in economies outside the Eurozone. In addition, investors are increasingly investing in alternative, illiquid asset classes such as private equity, private debt, real estate and infrastructure, which are often not EUR-denominated.

Consequently, currency risks have become a far-reaching and significant risk driver. Since currency positions are usually an unintentional by-product of intenational diversification and the currency risk taken is not systematically rewarded by a natural risk premium, hedging strategies are increasingly in demand. However, currency hedging can also have negative effects. A hedging strategy can have significant effects on liquidity and is expensive in the current market environment, for example when hedging the EUR versus the USD. Solving the conflict between market and hedging risks is a challenging issue. So how can currency risks be managed as efficiently and effectively as possible?

In many asset classes, the outsourcing of portfolio and risk management functions is a standard procedure. Increasingly, specialised managers are being hired for FX risks. They can effectively limit risks and achieve benefit through efficient management. The bundling of currency control with a central manager also offers considerable structural advantages that pay off in many ways for investors. This INSIGHT is intended to provide information on which factors must be taken into account in order to develop a strategy adapted to investors‘ needs. Additionally, passive and active currency overlay strategies will be presented. Since the efficiency of a currency overlay is essentially determined by its implementation, the key elements for this are outlined.

Factors influencing an individual hedging strategy

The aim of a hedging strategy is to manage and optimise the risk/return profile of currency positions in accordance with individual investor requirements. The first step in this process is a comprehensive analysis of the currency positions. The following investor-related factors must be taken into account:

Client‘s risk affinity/aversion

A key variable in the design of a hedging strategy is the risk-bearing capacity and preference of the investor. Their assessment requires the identification of the market and the liquidity risks of the existing currency positions.

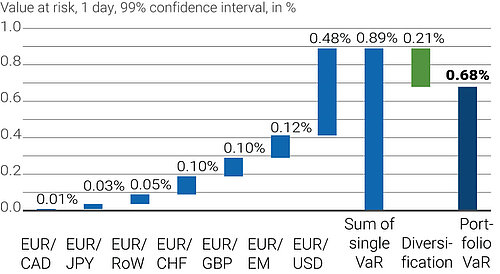

To this end, the potential loss resulting from a currency devaluation must be compared to the potential liquidity burden arising from the planned hedging transactions due to a foreign currency appreciation. For example, the analysis of the value at risk of the entire currency allocation shows both the economic risks of the unhedged currency portfolio and the diversification effects resulting from the allocation (see figure 1).

Fig. 1 | Value at risk of a typical FX portfolio

Source: 7orca Asset Management AG (30.04.2019)

The market risk of currency positions is determined in particular by currency-related volatility and the maximum loss risks from currency devaluations. In addition, currency effects should be assessed in connection with the underlying investment (see „Characteristics of the assets to be hedged“). The liquidity effects of a hedging strategy must also be compared with investor preferences. Negative market values of hedging instruments due to currency appreciation are problematic. If this affects liquidity, cash flows must be settled. These can consist of a liquidity reserve or through the timely liquidation of investments.

Characteristics of the assets to be hedged

The characteristics of the underlying asset must be included in the hedging strategy. Diversification effects between the currency and the underlying investment, which is largely determined by the correlations, should be taken into account. While investments denominated in foreign currencies also involve the risk of currency fluctuations, this volatility can also provide diversification effects. For example, historically the USD has often appreciated when market distortions have been severe. In such a phase, the negative performance of a USD-denominated asset can be cushioned by currency appreciation. In the case of underlyings that tend to have low volatility, such as bonds, the diversification effect is usually limited. Here, the currency volatility dominates the volatility of the investment.

If the currency risk stems from illiquid investments, such as real estate or private equity, it should be noted that liquidation is only possible to a limited extent. Additional liquidity reserves must be maintained for the hedging strategy. In the majority of cases, the mostly infrequent valuation of these investments means that changes in value are not detected promptly, which can lead to under or over hedging.

If the currency exposure were in turn the intended result of an investment decision by the investment manager of an underlying asset, a currency hedge would lead to an unwanted levelling of the alpha. This should be taken into account by the currency manager, for example by hedging the FX exposure of the specified benchmark.

Currency market environment

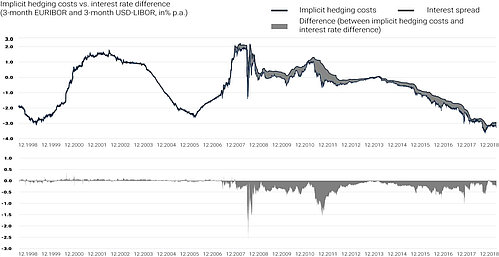

The market environment of individual currency pairs also has an impact on the design of the hedging strategy. In particular, the difference in interest rates between the investment and the home currency is an important aspect. The interest rate difference is paid out as part of a currency hedge. If there is a significant interest rate differential in two currency areas, e.g. currently 2.9% p.a. (Source: 7orca Asset Management AG, Bloomberg. EUR/USD forward spread approx. 2.9% p.a. in 3 month tenor. 30.04.2019) between the United States and the Eurozone, the interest rate differential to be paid out within the currency hedging strategy is particularly expensive. This also applies to the hedging of many emerging market currencies. In addition to different interest rate levels, the phenomenon of cross-currency basis spreads can also influence hedging costs. Put simply, it is a measure of the supply and demand ratio of two currencies and since 2008, it has been structurally negative for a EUR-based investor hedging USD holdings. This is an important factor, as it has a direct impact on the cost of a currency hedging strategy. In contrast to a higher interest rate level, an investor is not remunerated for the basis spread. In the USD example, the hedging costs paid exceed the interest rate differential between the two countries (see figure 2). If the investor has a strong market opinion on the development of currency pairs, this should be taken into account in the hedging strategy.

Fig. 2 | Hedging costs: interest spread vs. hedging costs

Sources: 7orca Asset Management AG, Bloomberg. (01.01.1998 – 30.04.2019)

Regulatory and infrastructural requirements

Furthermore, general regulatory requirements, such as MiFID II, MiFIR and EMIR, as well as specific ones, such as Solvency II, to which the investor is subject, should be addressed. In addition, the internal investment guidelines, a potential need for currency attribution and other reporting requirements play a role. This applies both to the individual adaptation and to the implementation of the investment process. The investor‘s existing infrastructure, such as the set-up of the master fund, and any direct holdings can have a significant influence on the hedging concept. A specialized currency manager can help with a comprehensive currency inventory and can use the results as an important basis for the design of hedging strategy.

The optimum hedging strategy

Currency overlay strategies outsourced to specialised managers allow a professional currency hedging. Currency overlay describes the management of currency risks detached from the basis investment using derivatives. It is adapted to the individual client situation. Depending on its requirements, they have a passive or active design. While in the passive version a defined, constant degree of protection of currency risks is implemented, this can be adjusted to market movements in active currency overlays.

Irrespective of the design, a central currency overlay manager that takes control of all currency positions of the client’s portfolio provides for the following structural advantages:

- A flexible structure is created, which allows a rapid and uncomplicated adjustment of all currency positions; e.g. in the event of a change in tactical or strategic asset allocation

- The increased level of transparency allows for improved measurability of the efficiency of the currency management

- The client has a contact person for all currency-specific topics

- Central liquidity management for currency hedging transactions minimises the cash position and reduces transaction costs due to any secondary transactions that may be necessary in the underlying assets

- Aggregated control of all currency positions allows netting effects to be leveraged (currency position rises in one segment and falls in another) and thereby the reduction of trading costs

Passive currency overlay

The primary objective of a passive currency overlay is to reduce the economic currency risk by minimising the currency-related volatility. A defined degree of hedging is maintained over time, taking into account fluctuations in the market value of the underlying assets. The focus is therefore on the efficient and cost-effective implementation of the hedging strategy and the outsourcing of operational activities. The overlay manager thus discharges the client or the manager of the underlying investment and achieves economies of scale. These arise because a central hedging is carried out across all currency positions. By integrating the following elements, a passive currency overlay can be further optimised:

Determination of the efficient deviation bands

Deviation bands define when a currency hedge needs to be adjusted for fluctuations in the market value of the underlying asset. If an adjustment is not made immediately, a portfolio is subject to currency fluctuations.

In this case, the portfolio is over or under hedged. The determination and use of efficient deviation bands enables an economically reasonable hedge through the reduction of the frequency of transactions and thus transaction costs.

Determination of the ideal hedge term

Passive currency overlay management can be further optimised by introducing a tenor management. This does not vary the degree of hedging of currency positions over time, but rather the term of the hedging instruments. The maturity structure diversifies the duration of the hedging instruments and reduces cash flow and counterparty risks. It is particularly important that the duration of the hedging instruments can be used to determine and optimise the costs of hedging. This is because the term of the instruments enables them to be positioned on the yield curves of two national economies.

Determination of the exposure

The consistency of a mandate is increased by determining the currency exposure across all positions. The calculation is based on the portfolio positions transmitted by the capital management company, the managers of the underlying investments or the investor. This enables a currency look-through and, if necessary, a remapping if the economic currency risk differs from the reporting currency.

Active currency overlay

A passive currency overlay minimises the economic currency risk at the price of not participating in positive currency developments. This symmetrical payout profile is attractive due to its simplicity, but falls behind the asymmetrical profile in sharply rising markets. Active currency overlay solutions enable the market-adaptive adjustment of the hedging degree: if currency risks dominate, a hedge is set up which is dissolved in the event of positive currency developments.

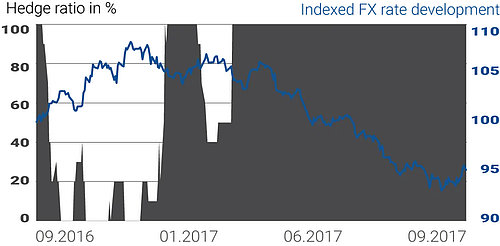

Figure 3 shows an example of the effect of an active currency overlay using a USD long position in the period from October 2016 to September 2017. This is a good illustration of the added value of an active hedging strategy. While the largely unsecured position clearly participated in the positive market development in the fourth quarter of 2016, the active build-up of the hedge at the end of 2016 largely protected the position until September 2017.

Fig. 3 | Functionality of an active currency overlay

Source: 7orca Asset Management (30.09.2019 –30.09.2017)

There are different approaches to the active management of currency risks. Discretionary and quantitative strategies, which have a fundamental or price-based design, contrast each other. Quantitative approaches enable replicable and consistent results in comparable market phases. This stable performance characteristic fulfils the premises of a purposeful risk management. In addition, it can be ensured that the investment process is not subject to any style drift. Compared to fundamental approaches, price-based approaches have the advantage that they are based on the market price, which represents the highest aggregation level of market information. This contains all information available on the market and establishes the clear causality between market price movements and hedging effects. Currency markets often evolve in an uncorrelated manner to other asset classes. They are influenced not only by the economic development of an economy, but also by how economies develop in relation to each other. Currency fluctuations are therefore sometimes very pronounced. The key to effective risk management lies in the correct identification of directional markets. Therefore, it is not the precise prediction of the future price level that is decisive, but the recognition of the market trend.

Investment processes, the core of which is the determination of market directionality, enable to achieve an asymmetric profile, similar to a put option on the foreign currency. In problematic market phases, this profile offers clients the greatest benefit. Although it is possible to represent an asymmetric profile by buying options, this strategy is uninteresting due to its high cost. This brings quantitative, price-based, directional approaches to the fore. These can generate such a profile more advantageously in the medium to long term: on the one hand, a more cost-effective long positioning is achieved in the realised volatility, and on the other hand aspects of behavioural finance can be integrated in order to generate more effective signals regarding the currency development.

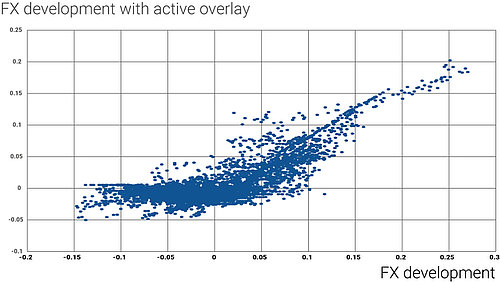

Figure 4 illustrates the relationship between foreign currency performance and foreign currency performance including active currency overlay. In principle, an active currency overlay should be adaptable so that the client‘s objectives and specifications are considered as precisely as possible in the strategy.

Fig. 4 | Fx development and active overlay strategy

Source: 7orca Asset Management AG (30.04.2019)

Integration of interest rate differential and machine learning

Against the background of the latest developments in research and information technology, active currency overlays should be continuously improved in order to meet changing market conditions and increasing customer needs in the future, too. This INSIGHT focuses on the integration of hedging costs into a quantitative investment process as well as the latest developments of selflearning programs, namely machine learning.

The consideration of hedging costs, which is determined in particular by the interest rate difference, is particularly important in the current market environment. The USD hedge, for example, is significant at approx. 3.15% p.a. (Source: Bloomberg, 7orca Asset Management AG. Interest rate difference of 2.9% p.a. (3-month EURIBOR vs. 3-month USD-LIBOR) plus 0.35% p.a. (hedging costs). 30.04.2019)

A mere tapping of the spot movement, i.e. the pure currency movement without the forward premium, would be too short-sighted. For example, the current interest rate differential and the resulting hedging costs would not be taken into account. Hedging should only be set up if it is expected that the devaluation of the currency will exceed the hedging costs.

Recent developments in the area of artificial intelligence have opened up new perspectives for alternative, data-driven model approaches. In contrast to traditional methods, these do not rely on pre-defined trade rules, but develop them autonomously via a data-supported selflearning process.

This approach is particularly advantageous when the dynamics of the underlying system are complex and difficult to describe – which is the case for price dynamics in the foreign exchange market. Neural networks are able to approximate almost any function. This enables them to discover even more complex relationships and patterns in the market data.

Implementation of the customised currency overlay

Once the client‘s currency hedging requirements have been defined and the design of a passive or active over lays has been determined, efficient implementation is the next step. This is an essential success factor for the currency overlay. The basis for efficient strategy implementation is the choice of hedging instruments, the guarantee of a robust best execution process and a combination of currency procurement and hedging.

Choice of instruments

The implementation via FX Futures or FX Forwards depends on the hedging requirements, the currency pairs and the corresponding liquidity in the respective instrument. In particular, large and complex mandates profit from of a combined solution. This structure ensures:

- Future security with regard to regulatory requirements and changed market conditions, since instruments of both categories can be used flexibly

- Use of both instruments ensures maximum market depth and best execution

- Selection of the hedging instrument with the lowest transaction costs and risks

- Diversified structure

The advantages of FX forwards lie in their flexible design with regard to the term and the hedging amount. Collateral is not necessarily required and good liquidity is provided for the majority of the currencies of developed countries and many emerging markets.FX futures are a very confident, exchange-regulated instrument. They convince through transparent execution, absence of counterparty risk and a standardised settlement and clearing process. FX futures are therefore ideal for hedging currencies of developed countries. In the case of a USD exposure, for example, the CME EUR/ USD future can be used, which has a daily average trading volume of approximately EUR 30 bn and thus offers very good liquidity. If there are „exotic“ currencies that do not have sufficient market depth, these can be hedged via FX forwards. Since there is a counterparty risk in OTC transactions, the selection of the liquidity provider is important. It is advisable to select the largest and most competitive brokers with a good rating. Here, too, a central currency overlay manager can achieve added value. On the one hand, he offers access to the most competitive liquidity providers on the market; on the other hand, he manages the broker relationships and the resulting credit risks in a structured manner.

Execution of the transaction

In order to obtain the necessary liquidity and the lowest transaction costs for an order, an extensive analysis is required in the run-up to a transaction. Although the currency market is very liquid, this liquidity is fragmented and there is no central marketplace.

Two factors in particular need to be considered here. On the one hand, the market impact, i.e. the influence on the market price, must be minimised. If an order is placed on the market too quickly, the market price can be impacted. However, if trading is too slow, the risk of adverse effects on the portfolio increases due to increased market risk, especially in the case of high volatility.

On the other hand, it is essential to monitor the signaling risk, i.e. the risk of informing the market of intended actions. In order to avoid this, algorithms can be used for executing orders. The trading process should be based on the life cycle of a transaction. Figure 5 illustrates the three phases of the cycle pre-trade, trade execution and post-trade.

| Pre-trade analysis | Trade execution | Post-trade analysis |

|---|---|---|

|

|

|

Fig. 5 | Life cycle of a transaction

The aim of a pre-trade analysis is to identify the strategy and trading time with the lowest transaction costs prior to trading, taking into account the current market depth and volatility. Once this has been done, trading is carried out with FX futures or FX forwards, analogous to the result. One of the objectives of the post-trade analysis is to monitor transaction costs and to develop derivations for future trading strategies.Exploiting economies of scaleAnother way to increase the efficiency of a currency overlay is to combine currency procurement and hedging. The aim is to align the currency procurement of the underlying segments with the hedging adjustment in the overlay segment. This approach enables market price risks to be eliminated as soon as they arise and transaction costs to be saved. Before implementation, it is necessary to check whether the processes of the manager of the underlying, of the capital management company and of the custodian need to be adjusted.

Exploiting economies of scale

Another way to increase the efficiency of a currency overlay is to combine currency sourcing and hedging. The aim is to synchronize the currency procurement of the underlying segments with the hedging adjustment in the overlay segment. This approach makes it possible to eliminate market price risks immediately when they arise and save transaction costs.

Before implementation, it is necessary to check whether the processes of the underlying investment manager, the capital management company and the depositary need to be adjusted.

Concluding consideration

As a result of the general increase in foreign currency exposure in institutional asset allocations, the central management by a specialised manager has a number of advantages. A currency overlay mandate incorporates the investor‘s individual requirements and ancillary conditions and is more than just an asset management mandate. It is also part of the infrastructure throughout its entire value chain.An overlay manager ensures that the client is always optimally positioned in the context of the continuous and structural change of the foreign exchange market. He is able to respond promptly to any changes.